WHY YOU SHOULD NOT BUY THE SPACEX IPO

Brought to you by The Millegans & The Woodworth Contrarian Fund

Sisyphus of Wall Street & The Weight of Hype: Why chasing marquee allocations is a rigged game—and what contrarians do instead.

Overview: Biggest IPO ever… for whom?

Every cycle, Wall Street dusts off the same script: the market is at all‑time highs, a "once‑in‑a‑lifetime" company files to go public, and banks line up to sell the story of the biggest IPO ever. For issuers and underwriters, that script works beautifully; for long‑term investors buying into the hype, the ending is usually much less inspiring.

The current round—headlined by a potential record‑breaking SpaceX deal—looks like a textbook late‑cycle IPO window: mega‑syndicates, breathless coverage, and buyers pledging billions before the ink is dry on the prospectus. History, and the data, both suggest the same contrarian response: let everyone else fight over the confetti; step in later when the valuation and the shareholder base are less emotional.

The SpaceX setup: late‑cycle IPO 101

Reporting on the planned SpaceX listing reads like a greatest‑hits album of IPO marketing: the largest deal ever, a roadshow pitched as an event, and a syndicate of more than 20 banks vying for a piece of the fee pool. Coverage notes that some investors have effectively pre‑ordered stock before seeing full financials, which is less due diligence and more concert ticket frenzy.

At the same time, there is chatter that OpenAI and other AI‑adjacent names could follow, turning 2026 into a blockbuster year for new issues after a relatively quiet stretch. When the calendar fills up like that, it usually signals that issuers—not buyers—are calling the shots on timing.

What really happens to IPOs after day one

Strip away the marketing, and IPOs share two uncomfortable facts. First, on average they pop on day one. Second, over the next few years they chronically lag the broad market. A Nasdaq review of U.S. IPOs found that nearly two‑thirds trailed the market by more than 10% three years after going public, despite an average first‑day gain of roughly 15–20%.

Academic work across markets tells the same story: long‑run IPO underperformance is persistent, especially among high‑sentiment, high‑volatility names that attract heavy retail attention. One study even shows a sizable slice of IPOs closing below issue price on day one, reminding everyone that "IPO" does not automatically mean "underpriced."

Marquee deals: great stories, awkward entry prices

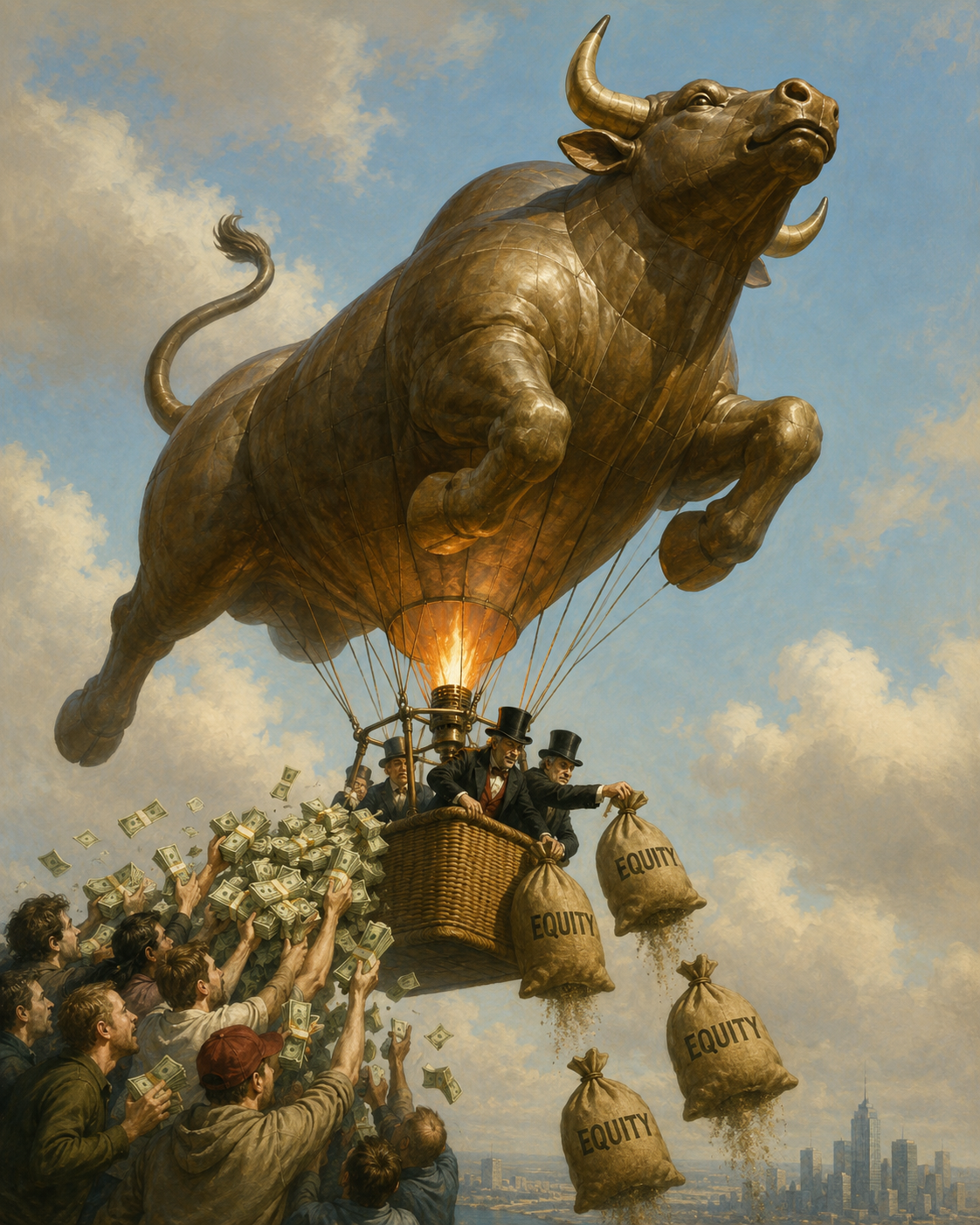

The Hot Air Bull: In the market for blockbuster deals, retail investors provide the heat, and insiders make the getaway.

Visa: perfect business, imperfect timing

Visa went public in 2008 at 44 dollars a share, raising about 17.9 billion dollars and briefly holding the record for largest U.S. IPO. The stock ripped higher on day one, trading north of 56 dollars and leaving billions "on the table" compared with where the market ultimately cleared that first session.

Visa has since been a terrific business and a strong long‑term compounder, but that is precisely the point: a great franchise did not need investors to pile in during the most crowded, most expensive 24 hours of its trading life. Patient buyers had multiple chances to own it at more reasonable multiples once the initial sugar rush wore off.

Facebook: from "must own" to "broken IPO" in a week

Facebook’s 2012 IPO raised about 16 billion dollars and was sold as a generational chance to own the social graph. Within days, the stock slipped sharply below its 38‑dollar offer price, closing around 34 dollars as trading glitches, valuation worries, and disappointment over the lack of a big first‑day pop all hit at once.

Anyone who bought the story instead of the numbers had to sit through a very public embarrassment; anyone who waited could buy the same company at a double‑digit discount with more information and less hysteria.

Alibaba and Saudi Aramco: record size, modest follow‑through

Alibaba’s 2014 New York listing raised roughly 22–25 billion dollars and delivered a storybook first day: priced at 68 dollars, it closed near 93–94 dollars, a gain of about 38% and more than 9 billion dollars of instant paper profit for deal participants. Saudi Aramco’s 2019 IPO pushed the record further, raising about 25–29 billion dollars and briefly valuing the company around 2 trillion dollars as local investors piled in.

Fast‑forward, and the narrative looks more muted. Aramco’s share price has mostly traded in a relatively tight band in local‑currency terms, with 52‑week ranges in the mid‑20 dollar equivalent and single‑digit percentage moves over many one‑year periods—hardly the stuff of "you had to be there on day one" legend. Alibaba has gone through its own boom‑and‑bust cycle, with plenty of chances to buy well below early post‑IPO highs once regulatory, macro, and competitive realities showed up.

General Motors: the big comeback that mostly trudged

GM raised more than 20 billion dollars in its 2010 return to public markets, including a large preferred component, and common shares opened just a couple of dollars above the 33‑dollar offer price. A decade later, coverage was comfortable calling the stock a "mediocre" investment relative to the broader market and sexier growth stories, despite all the drama of bankruptcy and rebirth.

Again, anyone desperate to own the "new GM" on day one was mainly locked in a pedestrian trajectory at a full recovery narrative price.

The structural tilt against long‑term buyers

Tilted Odds: Why the traditional virtues of patience and holding are ruthlessly penalized on a rigged board.

Issuers sell when the sun is shining

IPOs and monster follow‑on offerings are voluntary events. Companies and insiders pick their spots, and they almost never choose to sell big chunks of equity when markets are panicking and valuations are cheap. Reviews of mega‑deals like Aramco and Alibaba make this explicit: bankers and governments waited for strong equity markets and bullish sector sentiment before pulling the trigger.

If the seller has perfect timing and perfect information about their own business, it is worth asking why outside buyers should be racing to meet them at that moment.

Underwriters get paid on size, not your future returns

Banks make money on fees and on keeping their best clients happy, not on what happens to the stock three years after the IPO quietly leaves the front page. Academic work on Facebook’s pricing shows how, after an IPO that was perceived as "botched" because it failed to deliver a big day‑one pop, banks bent over backward to underprice the next wave of deals, showering trading profits on a short list of favored institutions.

The result: the fat part of the underpricing, when it exists, is captured by investors who reliably flip allocations and feed trading desks. Latecomers in the open market and long‑only funds trying to hold for years get whatever is left after that game is over.

The float is thin, the stories are thick

Most modern IPOs come to market with limited free float and a prospectus full of adjusted metrics and forward narratives. A growing majority of them are unprofitable at listing, which means buyers are asked to pay premium multiples on hoped‑for earnings several years out. In that environment, small changes in the story—one guidance cut, one regulatory headline—can have outsized effects on price.

When the float is thin, those price swings only get more violent until lockups expire and the shareholder base broadens.

Lockups: the second wave you can see coming

What lockups actually do

Lockup agreements bar insiders—founders, executives, employees, and pre‑IPO investors—from dumping stock for a set period, typically around 90–180 days after the IPO. The SEC highlights that six months remains the standard in many U.S. offerings, with details spelled out in the prospectus.

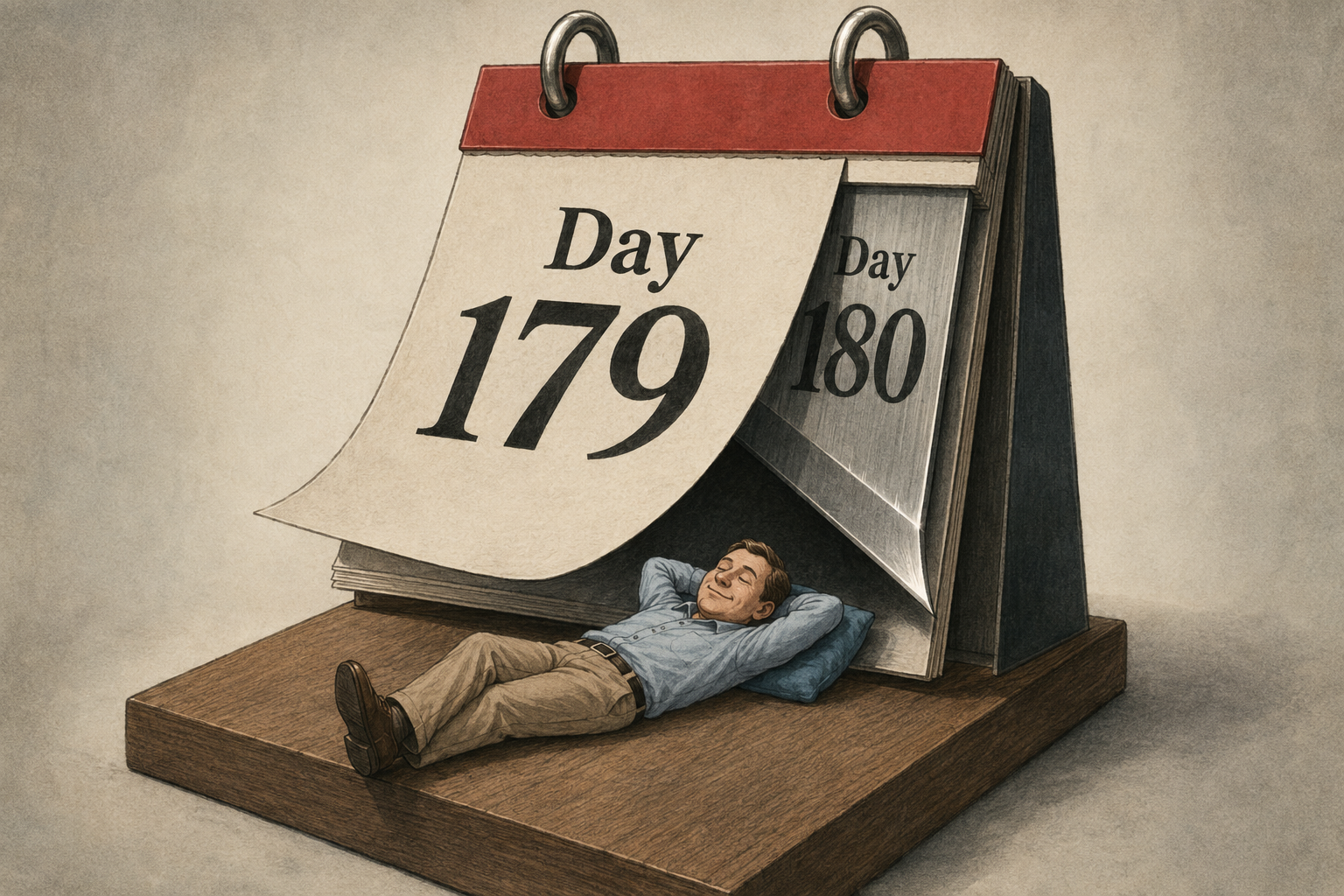

Sleeping under the 180-day blade: The post-IPO supply dump is a highly visible trap, yet retail capital always ends up on the chopping block.

The official story is that lockups promote an orderly market. The practical effect is that a huge block of stock is scheduled to become sale‑eligible on a known date, in size, regardless of where the price happens to be.

Why lockup expirations matter more than roadshows

When lockups roll off, early investors and employees who have waited years for liquidity finally get a chance to diversify. That is entirely rational for them—and potentially painful for anyone who just paid peak prices before a wave of technical selling.

Surveys of recent deals show more creative variations as well: staggered releases, price‑based triggers, and early‑release clauses in hot tech IPOs, all of which can create multiple windows of surprise supply. For a contrarian, the lockup calendar is often more interesting than the roadshow schedule.

What a contrarian does instead of chasing allocations

Beneath the Surface: While the crowd is dazzled by the flashy tip of an allocation, contrarians dive deep for unglamorous fundamentals.

Skip the casting call, show up for the rerun

The evidence on three‑year underperformance, thin floats, and lockup overhang all point to the same conclusion: there is rarely a structural reason for a long‑term, fundamentals‑driven strategy to insist on participating at the IPO price. The odds are better after earnings, after lockups, and after the story has met reality.

For a fund that makes its living buying what everyone else is ignoring, that means treating marquee IPOs as watch‑list candidates, not launch‑day emergencies. The work goes into understanding the business and the capital structure, then waiting for the first sentiment hangover instead of the first headline.

Respect the calendar: summer, elections, and thin liquidity

IPO windows do not exist in a vacuum. New issues tend to cluster after strong index runs and in seasons when institutions are actively deploying capital; they tend to struggle more in thin summer markets or around political events that can spike volatility. Layer a crowded deal calendar on top of a hot tape heading into a summer slowdown and a contentious election or midterm season, and the setup for new listings can get fragile fast.

In that environment, sidestepping IPO risk is less about missing out and more about refusing to underwrite other people’s timing.

The Woodworth playbook on IPOs

Put bluntly: marquee IPOs are usually fantastic for the companies selling stock and for the banks collecting fees, and a coin flip at best for the long‑term buyers paying up at the opening bell. A contrarian, valuation‑driven approach is more interested in the hangover than in the party.

That means:

Letting hype bidders set the first price, then revisiting the name once financials and incentives are clearer.

Tracking lockup expirations and secondary offerings as potential entry points when technical selling, not fundamentals, are driving price.

Being especially wary when the phrase "largest IPO ever" is doing the marketing heavy lifting.

When the market treats IPO allocations as lottery tickets, the contrarian advantage comes from declining the ticket and buying the business later—after the odds have quietly moved back in investors’ favor.

Further Reading

Wall Street Is Assembling Its Biggest IPO Syndicate Ever. - With the SpaceX roadshow weeks away, James Altucher makes the case that the obvious trade is not the...

What Happens to IPOs Over the Long Run? - Nasdaq - Three years after their IPO, we calculate that almost two-thirds of IPOs are underperforming the mar...

5 things to know about OpenAI's potentially record-breaking IPO plans - The maker of ChatGPT is preparing to go public in what could be the largest stock market debut in hi...

The Saudi Aramco IPO breaks records, but falls short of expectations - The Aramco IPO promised to be the largest ever, greatly surpassing the $25 billion offering of Chine...

SpaceX Is Aiming for Civilization on Mars. Its IPO Couldn't Be More ... - Appeared in the May 23, 2026, print edition as 'Spacex has Plans for mars, shares for humans What It...

Underpricing, underperformance and overreaction in initial public ... - We now approach the second stylized fact about IPOs – the long-term underpricing of the IPO firms co...

Factbox-From Saudi Aramco to Alibaba: World's biggest IPOs - WTAQ - If SpaceX raises the $75 billion it wants, the IPO would eclipse the world's largest to date, whic...

[PDF] “LONG-RUN PERFORMANCE OF INITIAL PUBLIC OFFERINGS ... - Academic research into firms that have gone public has been focused on the study of two anomalies: i...

IPO underperformance and the idiosyncratic risk puzzle - We find that IPO long-run underperformance is a manifestation of surprisingly low returns for high i...

How Common Are Negative First-Day IPO Returns? - We find that more IPOs with negative first-day returns occur at lower offer prices and smaller trans...

Capital Perspectives: SpaceX thoughts - The Journal Record - ... 23-24 WSJ by Corrie Driebusch and Ben Cohen titled “What it Takes to Launch the Largest IPO Ever...

Wall Street Gets a Taste of Blockbuster Stock-Market Debuts Ahead - Medline shares began trading under the ticker 'MDLN' Wednesday in the biggest IPO since 2021.

Visa Priced at $44 a Share, For Record $17.9 Billion - Visa, the world's largest credit card network, raised $17.9 billion in its initial public offering T...

Visa's $17.9B IPO sets a record on a bad day for stocks - ABC News - Shares of Visa gained so much their first day that the sellers missed out on a historic amount of mo...

Visa Inc. Prices Initial Public Offering - Visa - Investor Relations - (NYSE: V) announced today that it has priced the initial public offering of 406,000,000 shares of Cl...

IPO pricing as a function of your investment banks' past mistakes - On May 18, 2012 Facebook held its initial public offering (IPO), raising over $16 billion making it ...

IPO Pricing as a Function of your Investment Banks' Past Mistakes - On May 18, 2012 Facebook (FB) held its initial public offering (IPO) on NASDAQ, raising over $16 bil...

Facebook Plunges Below IPO Price in Frenetic Trading - Forbes - ... fell sharply below its $38 IPO price. The stock closed at $34.03, down about 11%. It was by far ...

FACTBOX-From Saudi Aramco to Alibaba: World's biggest IPOs - Analysts expect the potential landmark listing to reinvigorate the IPO market and push more high-pro...

Top 10 Largest Global IPOs of All Time - Investopedia - Saudi Aramco tops the list of global IPOs, raising $25.6 billion in December 2019.2 · Alibaba's IPO ...

The Biggest IPOs in History — and the One Everyone's ... - Instagram - Historic IPO Milestones: Saudi Aramco (2019) – $29.4B raised, world's largest IPO ever. Alibaba (...

Alibaba pops 38%, represents one third of 2014 IPO market proceeds - It priced at $68, which drove high demand as the stock began trading on the NYSE up 36% at $92.70 an...

Deals of the Year 2014: Alibaba Sets IPO Record with NYSE Debut - When Jack Ma appeared on the floor of the New York Stock Exchange on September 19 for the initial pu...

Alibaba Debut Makes a Splash - WSJ - The 38% first-day gain handed buyers of the offering paper profits of more than $9 billion and easil...

The Bigger Picture Behind The Aramco IPO - Forbes - Saudi Aramco's shares soared on their debut on the domestic stock exchange Wednesday, becoming the w...

Saudi Aramco Stock Price History - Investing.com - Saudi Aramco (2222) has delivered a 10.31% change over the past year, with a 52-week range between 2...

Please note that the Woodworth Contrarian Stock & Bond Fund, LP, of which the Millegan Brothers manage and are invested in, do not currently hold a position of SpaceX or SPCX as of the publication date of this article. They may or may not choose to modify their exposure to this name for any reason at any time. This is not a recommendation to buy or sell SpaceX/SPCX or any other name - investments incur significant risk, our risk tolerance may be significantly higher than the average investor, and any discussion in this article does not take into consideration your individual circumstances.

DEEP ROOTS. STUBBORN GROWTH. OREGON-BASED.

Now is a great time to diversify your portfolio with an investment into an award-winning fund. Call us or visit our website to inquire on an investment today in the Woodworth Contrarian Fund as an accredited investor.

(800) 651-1996 - info@woodworth.fund - www.Woodworth.Fund

Contrarian Value-Based Hedge Fund of the Year 2022-2026

Quinn Millegan (left) & Drew Millegan (right)

About the Managers: Brothers Drew Millegan and Quinn Millegan manage the Woodworth Contrarian Stock & Bond Fund, a hedge fund based in McMinnville, Oregon. They grew up in the finance world, and specialize in contrarian investment strategies in the US Public and Private markets.

Something missing from your portfolio may be a diversification into the Woodworth Contrarian Fund for accredited investors. Now is a great time to diversify your portfolio with an investment into a multi-award-winning fund. An exposure to a value-based contrarian strategy is a unique opportunity for your long term capital that you’re seeking aggressive returns for. With nine years of the Woodworth Fund under management, the Millegan Brothers are trained stock-pickers and experienced venture capital investors with a proven track record. Give us a call today to discuss a liquid investment with independent administration and independently audited monthly statements and a personal relationship.