THE MILLEGAN MEMO: POST-JANUARY 2026

Brought to you by The Woodworth Contrarian Fund

This month reads like three versions of the same story: whoever controls the bottleneck controls the scoreboard. In 1609, Isaac Le Maire tried to smack the Dutch East India Company back into its lane because monopolies eventually stop competing and start rewriting the rules. In 2026, Pinterest proved you can add users and print real GAAP profits, miss a revenue expectation by a hair, and still get publicly executed because ad buyers are spooked and the market is allergic to “maybe.” And the AI boom is taking that same logic into the physical world, turning electricity-linked land into a premium asset that can outbid housing—exactly why Oregon’s land-use system now looks less like a political quirk and more like a financial firewall.

— Managing Partners Drew Millegan & Quinn Millegan

“There’s no asset so good that it can’t be overpriced and become a bad investment, and very few assets are so bad they can’t be underpriced and be a good investment.”

WORM Index: January update

The Woodworth Oregon Market Index (WORM) finished January up ~1.4%, rising from 3,099.83 (12/31) to 3,143.10 (1/29), a gain of about +43.27 points. Same thesis as always: WORM’s job is not to be “right” every month, it’s to be a clean, Oregon-native scoreboard we can compound ideas against (and it is not the Woodworth portfolio, not reflective of our fund performance, and not an investable product).

One thing worth flagging in January’s tape is WORM’s high concentration of banks and community financials, which quietly makes the “Oregon tape” more rate- and credit-sensitive than people assume. In the current set, that bank cluster includes Summit Bank Group ($SBKO), BEO Bancorp ($BEOB), Oregon Pacific Bancorp ($ORPB), PBCO Financial Corporation ($PBCO), Citizens Bancorp ($CZBC), Oregon Bancorp ($ORBN), Pacific West Bancorp ($PWBK), and Lewis & Clark Bancorp ($LWCL). That matters because when banks are a chunky slice of the scoreboard, WORM can move on the boring-but-decisive stuff: deposit competition, loan growth, credit quality, and the direction of rates. And one housekeeping note: by the end of February, $LWCL will leave the index—the merger has already closed with Maps Credit Union, and any residual stock trading is essentially an artifact rather than a living, operating public company signal.

For clarity: WORM is a research/market-tracking index only; it does not represent what Woodworth is invested in, it does not track Woodworth returns, and you cannot buy it as a product. If you want the live level and the running archive, it’s all on the WORM page.

Pinterest (PINS): Growing, Profitable, and Still Punished

Pinterest got whacked after earnings for a very modern sin: the app did its job, the revenue line did not impress the spreadsheet gods. In Q4 2025, monthly active users climbed to 619M (+12% YoY), but revenue came in at $1.319B, a touch under what the market wanted, and that was enough to flip the switch from “nice growth” to “take it out back.” The funniest part is what gets ignored when the chart is yelling: Pinterest also posted GAAP net income of $277M for Q4 and $417M for full-year 2025. That’s not vibes, that’s profit. (investor.pinterestinc.com)

The near-term hangover is ad demand, and it’s not theoretical. Management and coverage pointed to retail advertisers pulling back under tariff pressure, which hits performance budgets fast when margins are already stressed. That fear bled straight into guidance: Pinterest’s initial Q1 2026 revenue outlook of $951M–$971M landed below consensus expectations and helped light the fuse on the post-print selloff. (Reuters)

That’s why we treated the drop as a value setup and took a position after earnings reset the price. Compared to the usual “attention economy” comparables, Pinterest is one of the few scaled ad platforms that is meaningfully profitable on a GAAP basis (again, $417M net income in 2025), while “peers” in the same sentence still struggle to produce consistent earnings. Snap, for example, logged a full-year 2025 GAAP net loss of $460M, even with better quarters. (investor.pinterestinc.com) In our view, compounding users plus real profitability plus a macro-driven selloff can create a stock trading below intrinsic value, even if tariff-jittery advertisers keep the next couple quarters messy. And notably, Pinterest raised its Q1 revenue forecast after the tvScientific acquisition, while trimming EBITDA guidance for integration and investment costs, which is a decent reminder the story isn’t “demand disappeared,” it’s “the mix got complicated.” (Reuters)

Please note that the Woodworth Contrarian Stock & Bond Fund, LP, of which the Millegan Brothers manage and are invested in, currently hold a position of PINS as of the publication date of this article. They may or may not choose to modify their exposure to this name for any reason at any time. This is not a recommendation to buy or sell PINS or any other name - investments incur significant risk, our risk tolerance may be significantly higher than the average investor, and any discussion in this article does not take into consideration your individual circumstances.

Take a look at our other January-printed stock reports you may have missed:

THE CHEMISTRY OF MISPRICING: WHY ADVANSIX (ASIX) IS A "DOLLAR FOR 50 CENTS"

METHODE ELECTRONICS (MEI): A Short Circuit or Just a Blown Fuse?

January in Economic History: 1609 - The First Activist Investor

Isaac Le Maire’s Portrait

On 24 January 1609, merchant-investor Isaac Le Maire woke up and chose violence—shareholder violence, the only kind that comes with ink, formal addresses, and a lethal amount of passive aggression. He fired off a written petition to Johan van Oldenbarnevelt and basically told the directors of the Dutch East India Company (VOC) to stop treating the company like their personal empire simulator. The board wanted to extend the VOC’s concessions and privileges; Le Maire’s response was: you’ve already tried to do too much, you’re not even executing your “true functions” properly, your privileges should be reduced, not expanded, and maybe—radical thought—there should be room for other companies to operate next to you. That’s an activist letter, four centuries before anyone could slap “activist” into a pitch deck.

Replica ship with VOC flag

The reason this little tantrum matters is that the VOC wasn’t just big; it was new. It was a state-chartered joint-stock corporation whose shares became the main event in Amsterdam’s secondary market, the closest thing the world had to a modern stock market that actually behaved like one—prices moving, liquidity forming, speculation arriving right on schedule. And the VOC’s 1602 charter explicitly opened participation broadly (commonly translated as residents being allowed to participate). Once you invite a wider public to buy in and trade, you don’t just get capital—you get a new social invention: strangers arguing about management decisions with money on the line.

So Le Maire’s 1609 petition is basically the first time you can watch the modern market machine spit out its inevitable byproducts: shareholders vs. insiders, ownership vs. control, and the awkward fact that a “public” company can also be a tool of state ambition. And it didn’t stop at strongly worded parchment. Le Maire and allies soon started trading VOC shares aggressively, helping trigger a political freak-out that contributed to Dutch authorities moving to restrict selling shares you don’t possess—an early, on-the-nose panic about short selling. The whole episode is the oldest version of a story we still watch every quarter: someone calls out management, the stock becomes a battleground, and regulators show up right after the shouting gets loud enough.

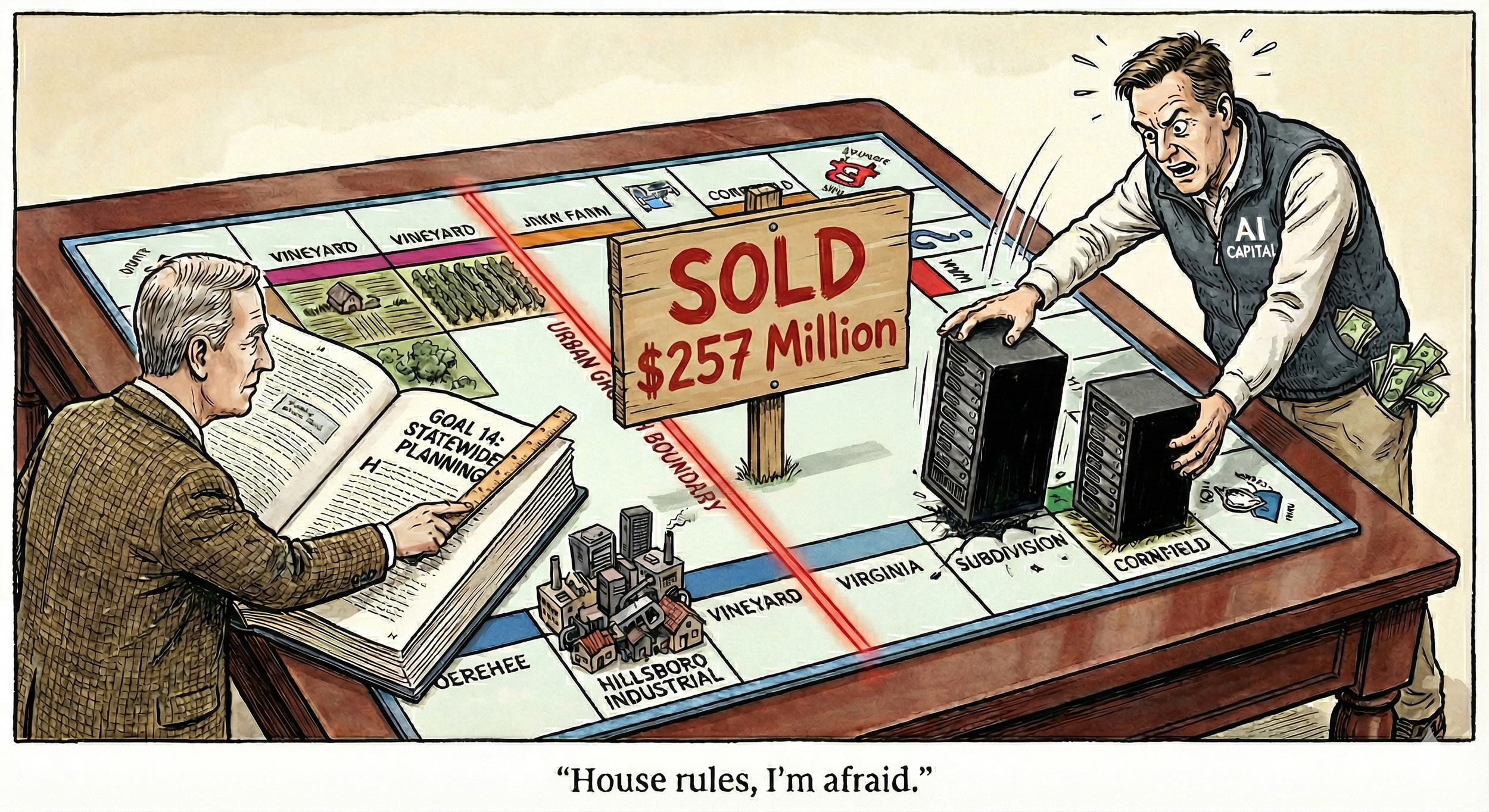

Servers Ate My Subdivision

The AI boom is turning “powered dirt” into the new oil, and it’s starting to mug housing for the land. The The Wall Street Journal reported a Northern Virginia example where a homebuilder planning 516 homes in Bristow watched surrounding parcels get snapped up by data-center demand, with Microsoft and Google cited among the buyers circling the area—and one nearby housing-intended site (approved for 250 units) ultimately sold to a data-center developer for $31 million, followed later by NTT paying $257 million for additional vacant acreage. (The Wall Street Journal) The market point is simple: when AI turns electricity access into a competitive advantage, data centers can outbid housing because they’re buying a long-duration cash-flow machine, not just lots and drywall.

Now put an Oregon lens on it: our land-use system is basically designed to prevent “highest-bidder sprawl” from bulldozing the map. Oregon’s unique land-use laws & statewide planning framework (Goal 14) requires urban growth boundaries and explicitly aims to accommodate urban population and employment inside those boundaries while pushing efficient land use—translation: growth gets funneled into urban densification rather than letting every new boom pick off rural land at will. (Oregon) This is why we have the world-acclaimed Oregon wine industry instead of suburbia and why the Millegan Brothers were able to get Pegasus Equestrian approved on over 2,800 acres. All that said, it doesn’t make Oregon immune to the AI land grab; it just changes the battleground from “subdivisions getting outbid in cornfields” to “industrial land scarcity inside the boundary,” where every expansion becomes a political knife fight—exactly the dynamic showing up right now in the Hillsboro-area debate over attracting more tech/industrial development versus protecting farmland. (opb.org)

DON’T FOLLOW THE CROWD. CALL US TODAY & INVEST CONTRARIAN.

If you’re seeking liquid access to institutional insights within a hands-on managed, direct investment portfolio featuring differentiated strategies, the Woodworth Contrarian Fund is open to new capital. We prioritize personalized service and building lasting relationships with our investors — because your goals deserve tailored attention and transparent communication.

Ready to explore how our contrarian approach can complement your portfolio? Reach out directly to our team for detailed fund information, eligibility for accredited investors, and next steps.

Stay informed by subscribing to the Millegan Memo and listening to the Capital Call podcast, where we share timely perspectives and in-depth market analysis.

Your next investment opportunity begins with a conversation — contact us today to learn more.

DEEP ROOTS. STUBBORN GROWTH. OREGON-BASED.

Now is a great time to diversify your portfolio with an investment into an award-winning fund. Call us or visit our website to inquire on an investment today in the Woodworth Contrarian Fund as an accredited investor.

(800) 651-1996 - info@woodworth.fund - www.Woodworth.Fund

Contrarian Value-Based Hedge Fund of the Year 2022-2024

Quinn Millegan (left) & Drew Millegan (right)

About the Managers: Brothers Drew Millegan and Quinn Millegan manage the Woodworth Contrarian Stock & Bond Fund, a hedge fund based in McMinnville, Oregon. They grew up in the finance world, and specialize in contrarian investment strategies in the US Public and Private markets.

Something missing from your portfolio may be a diversification into the Woodworth Contrarian Fund for accredited investors. Now is a great time to diversify your portfolio with an investment into a multi-award-winning fund. An exposure to a value-based contrarian strategy is a unique opportunity for your long term capital that you’re seeking aggressive returns for. With nine years of the Woodworth Fund under management, the Millegan Brothers are trained stock-pickers and experienced venture capital investors with a proven track record. Give us a call today to discuss a liquid investment with independent administration and independently audited monthly statements and a personal relationship.