THE MILLEGAN MEMO: SEPTEMBER 2025

Brought to you by The Woodworth Contrarian Fund

Helen of Troy (HELE) is cheap, wheat commodity corners collapse in 1871, the Woodworth Fund releases its Q3 Newsletter, and the yield curve flips back. Different centuries, same story: the market always humbles someone.

— Managing Partners Drew Millegan & Quinn Millegan

“No man ever steps in the same river twice, for it’s not the same river and he’s not the same man.”

HELEN OF TROY (HELE): A $70 BALANCE SHEET IN A $26 DRESS

Helen of Troy by Evelyn De Morgan (1898, London)

Helen of Troy remains an oversold gem. A seller of a variety of home and cleaning products, the company has pulled back over the course of 2025 from the $60 range to less than $26 per share. However, both earnings and the balance sheet of the company remain remarkably strong. On assets alone, HELE not only commands a solid valuation of $73.65 per share, which has grown over the course of its price decline, while its debt to capital remains below 31% as of last report. Most recent earnings, though down nearly 85% quarter over quarter, are still solidly positive and projected to recover absent unforeseen circumstances. On a fundamental basis, the discount is truly eye-popping.

Jitters over Chinese business and tariffs made be overdone. The market continues to heavily discount HELE relative to its underlying value and growth in large part because, firstly, it has global exposure and specifically outsized exposure to the Chinese market and, secondly, because it is exposed to the vagaries of consumer spending. Retail companies as a whole have faced headwinds from broad global economic uncertainty. However, Helen of Troy did something novel in the face of these issues - it shortened and shifted its supply chains. Much of their product slated for sale in the US has now shifted manufacturing to friendlier non-Chinese countries, and Chinese production in turn has been shifted to sell into non-US markets. This isn’t a foolproof plan, and it has come with costs, but it has kept the company earnings more solidly in the black than many analysts expected at the cost of a short-term hit to their bottom line. Consumer spending, for its part, has also remained remarkably robust, despite pullbacks in producer purchasing. This is one of those companies that has an eye on long-term reward and consequence, even if the market punishes them in the short-term.

HELE’s next earnings report is slated for Thursday, October 9th, which will partly determine whether or not we will eat our hats over this news release. Nothing is guaranteed in the markets. The Woodworth Fund maintains a position bought in July at an average cost basis of $22.14. Based on our proprietary fundamental & technical analysis, the company could easily break out from here. With a long term time horizon in mind, we could easily see HELE above $60. As such, it is still a buy in our opinion.

Please note that the Woodworth Contrarian Stock & Bond Fund, LP, of which the Millegan Brothers manage and are invested in, currently holds a position of HELE as of the publication date of this article. They may or may not choose to decrease or increase their exposure to this name for any reason at any time. This is not a recommendation to buy or sell HELE or any other name - investments incur significant risk, our risk tolerance may be significantly higher than the average investor, and any discussion in this article does not take into consideration your individual circumstances.

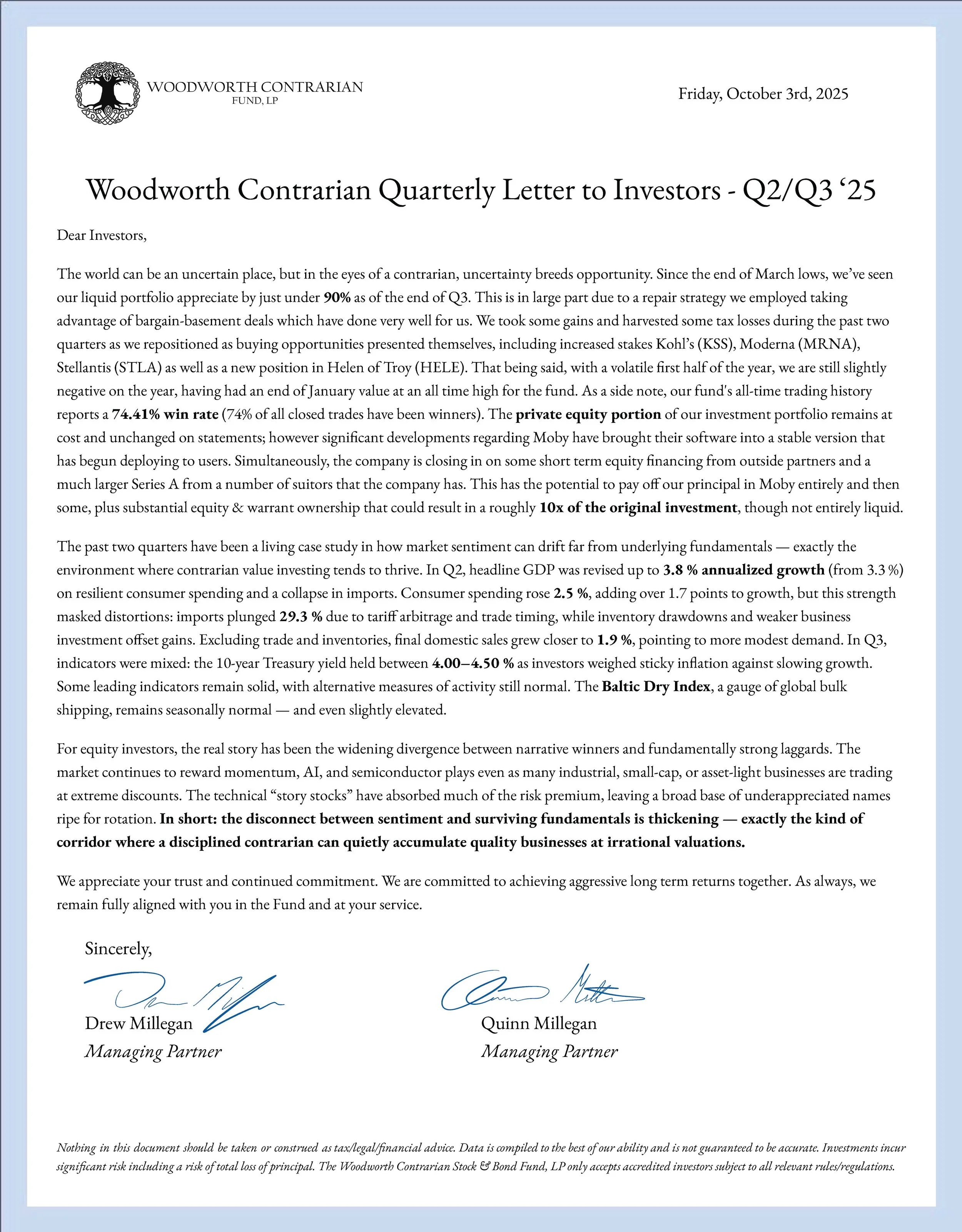

Q3 2025 WOODWORTH CONTRARIAN FUND INVESTOR NEWSLETTER

The Woodworth Fund has released its latest quarterly newsletter. We will let this one speak for itself!

Click here to view the article in a larger format.

SEPTEMBER IN ECONOMIC HISTORY: CHICAGO’S WHEAT KINGS, TOPPLED BY 567 TRAIN CARS - THE GREAT WHEAT CORNER OF 1871

In late summer 1871, a handful of Chicago speculators thought they could play god with grain. They snapped up nearly 2 million bushels of No. 2 spring wheat, using “seller’s option” contracts to choke off supply. For a moment, it looked like they had the market in a vice — prices for September wheat climbed 10 cents above later deliveries, and the syndicate dreamed of pocketing $140,000 (a fortune in those days) at the expense of the “unwary shorts.”

But wheat doesn’t grow on ledgers; it grows in fields. Within days, farmers rolled into Chicago with 567 carloads of fresh harvest, and more kept arriving. The speculators, forced to buy every load to maintain their corner, found themselves drowning in their own scheme. What had been a tidy squeeze turned into an endless obligation — pay inflated prices now, lose when you can’t unload later.

The New York Times reported that four out of five attempts to corner commodity markets in Chicago over the prior decade had failed, and this one was already heading that way. Farmers who sold promptly got to cash in; everyone else — speculators and stubborn holders alike — would watch prices collapse.

The folklore of these corners is delicious: the image of proud city wheat-kings undone by the unstoppable tide of Midwestern wagons, farmers laughing as they broke the market with nothing more than their harvest. The truth was less romantic: corners were technical manipulations that rarely succeeded, usually left wreckage in their wake, and destabilized prices for the very agricultural community they preyed upon. But the legend stuck — greedy speculators can corner all the old wheat in warehouses, but they can’t corner the prairie.

YIELD CURVE FLIP AND WHAT IT MEANS (PERPLEXITY-DRIVEN ARTICLE)

The U.S. Treasury yield curve has normalized to a 10-year/2-year spread of 0.57% as of October 2025 after inverting from July 2022 through August 2024, making it the longest inversion on record. Short-term rates (3-month: 4.01%, 2-year: 3.55%) remain below longer-term rates (10-year: 4.12%, 30-year: 4.72%), and the current spread is still slightly below its long-term average of 0.85%. Historical precedence shows yield-curve inversions typically precede recessions by 6–24 months, and with the recent inversion ending in August 2024, recession probability models remain elevated: the New York Fed’s 10-year/3-month model signals a 57% chance of recession within a year, while alternative indicators range from 20% to 45%.

The steepening of the curve signals markets expect rate cuts and eventual economic stabilization, but the historically tight spread and elevated recession probabilities suggest recession risk remains above normal. Unlike 2007, today’s banking sector is healthier and the Fed has more policy flexibility, increasing the odds of a soft landing — but given the typical lag between inversion and downturn, vigilance is warranted as the economy navigates potential headwinds through 2025. For a more detailed analysis - see the original article here.

DON’T FOLLOW THE CROWD. CALL US TODAY & INVEST CONTRARIAN.

If you’re seeking liquid access to institutional insights within a hands-on managed, direct investment portfolio featuring differentiated strategies, the Woodworth Contrarian Fund is open to new capital. We prioritize personalized service and building lasting relationships with our investors — because your goals deserve tailored attention and transparent communication.

Ready to explore how our contrarian approach can complement your portfolio? Reach out directly to our team for detailed fund information, eligibility for accredited investors, and next steps.

Stay informed by subscribing to the Millegan Memo and listening to the Capital Call podcast, where we share timely perspectives and in-depth market analysis.

Your next investment opportunity begins with a conversation — contact us today to learn more.

DEEP ROOTS. STUBBORN GROWTH. OREGON-BASED.

Now is a great time to diversify your portfolio with an investment into an award-winning fund. Call us or visit our website to inquire on an investment today in the Woodworth Contrarian Fund as an accredited investor.

(800) 651-1996 - info@woodworth.fund - www.Woodworth.Fund

Contrarian Value-Based Hedge Fund of the Year 2022-2024

Quinn Millegan (left) & Drew Millegan (right)

About the Managers: Brothers Drew Millegan and Quinn Millegan manage the Woodworth Contrarian Stock & Bond Fund, a hedge fund based in McMinnville, Oregon. They grew up in the finance world, and specialize in contrarian investment strategies in the US Public and Private markets.

Something missing from your portfolio may be a diversification into the Woodworth Contrarian Fund for accredited investors. Now is a great time to diversify your portfolio with an investment into a multi-award-winning fund. An exposure to a value-based contrarian strategy is a unique opportunity for your long term capital that you’re seeking aggressive returns for. With nine years of the Woodworth Fund under management, the Millegan Brothers are trained stock-pickers and experienced venture capital investors with a proven track record. Give us a call today to discuss a liquid investment with independent administration and independently audited monthly statements and a personal relationship.