SWIPED LEFT BY WALL STREET: THE BMBL REBOUND TRADE

Brought to you by Drew Millegan & The Woodworth Contrarian Fund

Bumble looks like another “dead app” stock at first glance—revenue rolling over, consensus price targets drifting down, and big tech funds ghosting it like a bad first date. Under the hood, it is a turnaround in mid‑flight: cutting costs hard, consolidating assets like Fruitz and Geneva, and putting the founder back in charge at a price that bakes in way more heartbreak than the current business performance justifies.

From busted IPO to rebound candidate

When Bumble went public in February of 2021, it was the market’s shiny new match—women‑first, high‑growth, all vibes. It priced at $43, above the initial range of $28-$30 and revised range of $37-$39 and then closed up over 60% on its first day.

Now it trades in the single digits around $3.50, lumped in with busted SPACs and apps people swear they deleted.

The headline: Q3 2025 revenue came in around $246 million, down about 10% year‑over‑year, with management guiding to another 14–17% drop in Q4 as they tighten the ecosystem and de‑risk lower‑quality monetization. Analysts have responded like spurned exes, trimming targets and fretting that the dating category itself is aging out.

But look at the actual relationship math: in that same Q3, Bumble produced roughly $52 million of net income and about $83 million of adjusted EBITDA, a margin near 34% versus roughly 30% a year earlier. That is not a dying fling; it is a business deliberately trading some near‑term growth for better‑quality revenue and fatter margins.

The hard reset: fewer bodies, better body

Bumble hasn’t tried to “it's not you, it’s macro” its way through this. It has done the unsexy work of a real reset.

Roughly 30% of the workforce has been cut as part of a turnaround plan to streamline, free up cash, and point resources at core priorities like AI and the flagship Bumble app.

Management has described a focus on pruning underperforming pieces of the business and concentrating spend where it actually moves the needle on retention and monetization.

The result shows up quarter‑on‑quarter: even with revenue down double digits versus the prior year, adjusted EBITDA margin expanded into the mid‑30s, reflecting cost saves and mix shift.

Quarterly comps tell the story the market is ignoring: year‑over‑year, Q3 revenue is lower, but profitability is better and the cash engine is running hotter, not colder. It’s like someone went from three chaotic situationships to one stable relationship with actual savings—less headline excitement, better long‑term outcome.

Founder back, product first, then monetize

Co-founder and CEO of Bumble Whitney Wolfe speaks onstage during TechCrunch Disrupt NY 2016 at Brooklyn Cruise Terminal on May 11, 2016 in New York City. (Photo by Noam Galai/Getty Images for TechCrunch)

The board also hit the leadership panic button in a way that actually makes sense.

After handing the CEO job to Lidiane Jones, Bumble announced in January 2025 that founder Whitney Wolfe Herd (Fun fact: also a co-founder of Tinder, the youngest female self-made billionaire, & the youngest woman to take a company public in the US) would return as CEO in March to drive the next phase of transformation.

A refreshed senior bench—including a new CFO and a Chief Business Officer—has been tasked with making the financials and product roadmap match the mission again.

Strategically, the playbook is:

Fix user experience and safety first (better matching, better AI‑driven moderation), then lean back into growth and ARPPU (Average Revenue Per Paying User) once the app feels less like a red‑flag factory.

Treat Bumble as a portfolio, not a one‑app wonder: Bumble, Badoo, Bumble for Friends, and other modes share core tech and can cross‑pollinate engagement.

On a quarter‑to‑quarter basis, that means living with ugly top‑line comps while the product team rips out bad plumbing. In dating terms: they’re doing the therapy and deleting a few toxic contacts before re‑downloading anything.

Fruitz, Geneva, and the hidden address book

The market still talks about Bumble like it’s just “that one yellow app,” but there is more in the phone.

Badoo: Long before the IPO, Bumble’s parent acquired Badoo, a mass‑market, international dating and social‑discovery platform with particular strength in Europe and Latin America, giving the group broad geographic reach and a different demographic mix than the flagship app.

Fruitz: Acquired in 2022, a fast‑growing Gen Z app in France and other European markets that uses fruit icons to clarify intentions—Bumble’s way of securing a younger, international demo.

Official and related tools: Relationship‑tracking and engagement apps that extend the monetizable life of a match beyond the first swipe.

Geneva: Signed and then closed in 2024, a group/community platform with chat, audio, video, and broadcast features, giving Bumble infrastructure for friend groups and interest‑based communities, not just one‑to‑one chats.

Taken together, Bumble now controls a network that stretches from first contact (Bumble/Fruitz/Badoo) to friendships (Bumble for Friends, Geneva) to ongoing relationships (Official), all running on a shared data and safety stack. Quarterly numbers today barely credit these assets; they mostly show up as cost and integration noise while monetization lags.

That is the kind of ecosystem that tends to be mispriced when investors are doom‑scrolling only one KPI (revenue growth) quarter‑over‑quarter.

Valuation: Priced Like a Bad Breakup

On the numbers, the market is valuing Bumble like someone who just got dumped via text—way more pessimistic than the relationship history supports. Recent data put Bumble’s market cap in roughly the $400–425 million range, with enterprise value around $1.06 billion, against about $1.03 billion in trailing‑twelve‑month revenue. That implies a Price/Sales multiple of about 0.5x and an EV/Sales multiple around 1.03x, levels usually reserved for ex‑growth industrials, not asset‑light consumer‑internet platforms with mid-30s adjusted EBITDA margins in the latest quarter.

The balance sheet makes that disconnect more interesting. As of 2025, Bumble carries roughly $1.13 billion of goodwill and another $0.59 billion of intangible assets, for total goodwill‑and‑intangibles around $1.72 billion—far in excess of today’s equity value. Goodwill is the accounting plug between purchase price and the fair value of acquired net assets; in normal‑person terms, it is what you pay for brands, networks, and other hard‑to‑measure relationship capital when you buy a business. Right now the market is saying those accumulated relationship assets—Badoo, Fruitz, Official, Geneva, plus the core Bumble brand—are worth cents on the dollar of what Bumble has paid and invested over the years.

On standard ratios, third‑party services peg Bumble at roughly 0.53x Price/Sales, 0.58x Price/Book, and about 2.89x Price/Free Cash Flow, with a forward P/E near 5.36x, all of which sit well below sector medians and far below where most “ok, not great” consumer internet platforms trade. That’s the market treating a one‑time reset of goodwill value and a bruised narrative as if the whole franchise has permanently lost its mojo, rather than just taking an optical hit while the cash engine keeps running.

Relative Valuation: Bumble vs the Rest of the Dating Pool

Compared to its peers, Bumble is the date who showed up five minutes early with a solid job and a plan—so the market assumes it’s boring and goes chasing the louder mess across the bar.

Sector context: Across public online‑dating and interactive‑media names, revenue multiples typically run between 0.7x and nearly 2x, with EV/EBITDA often in the low‑ to mid‑teens once investors believe the story. Bumble, at ~0.4x sales and a single‑digit implied EBITDA multiple, is well below that “this is at least fine” band.

Match Group (MTCH): Match carries goodwill around $2.3 billion and total goodwill‑and‑intangibles around $2.5 billion, reflecting the price paid for Tinder and other brands, and still trades at substantially higher revenue and earnings multiples than Bumble. Investors are effectively saying Match’s acquired love life deserves a premium multiple while Bumble’s deserves a discount, despite both operating in the same messy dating pond.

Grindr (GRND): Grindr, another pure‑play dating name, has historically traded closer to or above 1x sales with a premium for niche dominance and growth, even with a far narrower demographic footprint than Bumble’s global portfolio.

Peer screens that line up BMBL vs Interactive Media & Services broadly show Bumble’s 0.53x Price/Sales and 0.58x Price/Book sitting at a steep discount to the 1–2x revenue and 1.5–3x book ranges common for the group. Meanwhile, those same screens acknowledge Bumble’s profitability and cash generation as at least in line, if not better, than the median small‑cap peer. In dating‑app terms: the market is paying full freight for the obvious “hot” profiles (Match, Grindr) and slapping a clearance‑rack sticker on the one that actually has a stable job, decent income, and more relationship history baked into goodwill.

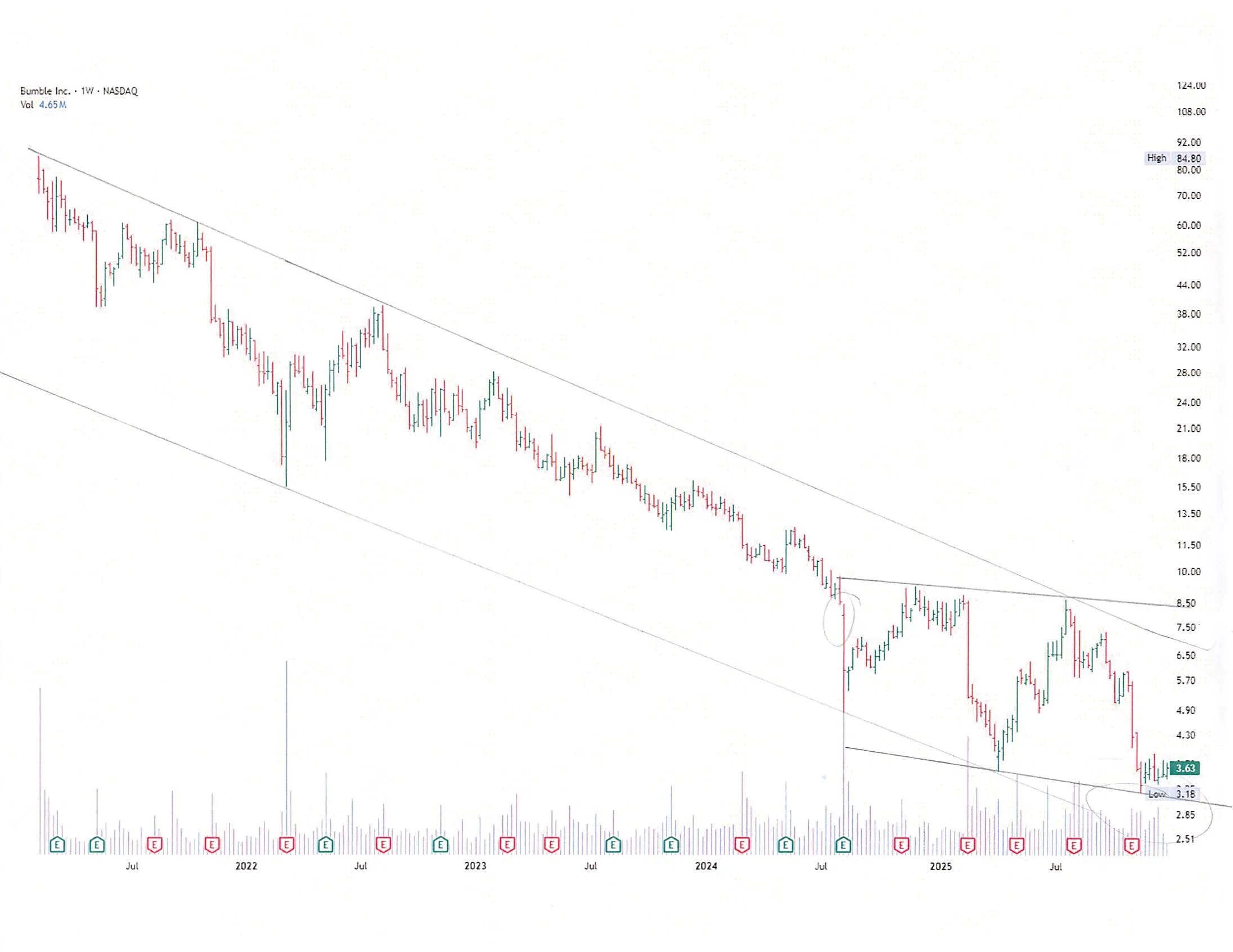

Technicals: The Chart Everyone Swiped Left On

BMBL All-time Chart

BMBL 3 Year Chart

BMBL 1 Year Chart

If the fundamentals read like a messy situationship, the chart looks like the morning after. Over 12 months, Bumble has slid from a 52‑week high near the high single digits down toward the mid‑$3s, a drop of roughly 60%, with the 52‑week low around $3.55. Recent closes sit much closer to that low than to the prior high—classic Clifford Pistolese territory for “disappointment fully discounted, seller enthusiasm exhausted.”

Pistolese’s book Using Technical Analysis: A Step‑by‑Step Guide to Understanding and Applying Stock Market Charting Techniques lays out a simple idea: watch trendlines, trading ranges, and volume to see when a stock is moving from distribution (better‑informed sellers bailing) to accumulation (better‑informed buyers quietly loading up). On a 1‑year view, BMBL’s price path fits his “extended decline, tentative base” template: a sharp fall into the $3–4 zone, then choppy sideways action with shrinking swings and early signs of a trading range rather than a straight‑line downtrend. Support has started to show up around the prior low, while any bounce back toward $5–6 runs into old breakdown levels—exactly the kind of range where weak‑hand sellers hand shares to slower‑money contrarians.

Stretch that to three and five years and you get the full bad‑breakup saga: a long sequence of lower highs and lower lows from IPO‑era levels into single digits, with multi‑year underperformance versus the indices and heavy volume trading near the recent lows. In Pistolese’s language, that kind of multi‑year washout plus base‑building is what you look for when “most of the emotional selling has already happened” and the ownership base has quietly shifted from momentum chasers to long‑only gluttons for punishment.

Mispriced like a bad date, not a bad business

Put the fundamentals, the goodwill pile, the peer comps, the valuation, and the chart together and the disconnect gets louder. At a mid‑single‑digit stock price hugging multi‑year lows, trading at a steep discount to both sales and book and with billions of dollars in goodwill and intangibles from past acquisitions sitting on the balance sheet, the equity is being treated like a serial cheater: everyone assumes the next quarterly surprise will be worse, not better.

One popular risk gauge, the Altman Z‑Score, pegs Bumble around 0.76, comfortably below the 3.0 line most textbooks call “safe.” The Altman Z‑Score is a composite formula that combines profitability, leverage, liquidity, solvency, and activity ratios into a single number to estimate bankruptcy risk; scores below about 1.8 are often labeled “distress,” while scores above 3.0 are seen as healthy. In Bumble’s case, that number is being read as a scarlet letter, even though:

Q3 2025 delivered positive net income and mid‑30s adjusted EBITDA margin versus a lower margin a year earlier.

A Piotroski F‑Score around 7 suggests improving profitability and operating efficiency.

External estimates put the cost of equity at roughly 7.5%, which is not where true basket‑case small‑caps trade.

Peer comps and sector averages say investors routinely pay 1–2x revenue for similar dating and interactive‑media platforms, not 0.5x, and they usually don’t get this much accumulated goodwill and intangibles for free.

In other words, the story looks like a rebound‑relationship cliché, the chart looks like the aftermath of a brutal breakup, the valuation looks like the market has priced in permanent celibacy, and the goodwill line says Bumble has spent years building and buying relationship assets the stock price is now essentially writing off. The price action says the emotional selling is largely done; the multiples and Altman Z say the market is still sulking; the fundamentals and asset base say the business is still very much in the pool.

Conclusion: Targeting a Healthier Relationship

Putting a number on all this, a reasonable base‑case target assumes:

Revenue declines moderate over the next 12–24 months and then flatten, with low‑single‑digit growth resuming off a lower base.

EBITDA margins normalize in the low‑30s rather than the mid‑30s peak seen in Q3, reflecting some reinvestment into product and marketing.

The market is eventually willing to pay 1.0–1.2x EV/Sales and a high‑single‑digit to low‑teens EV/EBITDA multiple—still a discount to where more loved dating and interactive‑media platforms trade, but no longer a “this thing is over” tag.

On roughly $1 billion of sales, a 1.0–1.2x EV/Sales band implies enterprise value of $1.0–1.2 billion. Netting out current net debt and cash leaves room for an equity value in the $900 million–$1.1 billion range, versus an implied ~$400 million today, or roughly $8–10 per share depending on share count and buyback behavior—about 2–3x the recent mid‑$3s trading level.

That price target does not require Bumble to become the next Meta of dating; it only requires the market to concede that an app with positive net income, mid‑30s EBITDA margins, billions of dollars of accumulated goodwill and intangibles, and a founder‑led turnaround probably deserves to trade like a bruised going concern rather than a failed experiment. For investors willing to live through a few more awkward quarters, BMBL at current levels looks less like a doomed relationship and more like a deeply discounted second chance—one where the odds of asymmetry skew in favor of those still willing to swipe right.

Disclosure: This analysis is for informational purposes only. Position sizing, timing, and risk management are essential. Do your own due diligence.

Please note that the Woodworth Contrarian Stock & Bond Fund, LP, of which the Millegan Brothers manage and are invested in, currently hold a position of BMBL as of the publication date of this article. They may or may not choose to modify their exposure to this name for any reason at any time. This is not a recommendation to buy or sell BMBL or any other name - investments incur significant risk, our risk tolerance may be significantly higher than the average investor, and any discussion in this article does not take into consideration your individual circumstances.

DEEP ROOTS. STUBBORN GROWTH. OREGON-BASED.

Now is a great time to diversify your portfolio with an investment into an award-winning fund. Call us or visit our website to inquire on an investment today in the Woodworth Contrarian Fund as an accredited investor.

(800) 651-1996 - info@woodworth.fund - www.Woodworth.Fund

Contrarian Value-Based Hedge Fund of the Year 2022-2024

Quinn Millegan (left) & Drew Millegan (right)

About the Managers: Brothers Drew Millegan and Quinn Millegan manage the Woodworth Contrarian Stock & Bond Fund, a hedge fund based in McMinnville, Oregon. They grew up in the finance world, and specialize in contrarian investment strategies in the US Public and Private markets.

Something missing from your portfolio may be a diversification into the Woodworth Contrarian Fund for accredited investors. Now is a great time to diversify your portfolio with an investment into a multi-award-winning fund. An exposure to a value-based contrarian strategy is a unique opportunity for your long term capital that you’re seeking aggressive returns for. With nine years of the Woodworth Fund under management, the Millegan Brothers are trained stock-pickers and experienced venture capital investors with a proven track record. Give us a call today to discuss a liquid investment with independent administration and independently audited monthly statements and a personal relationship.